Given that CPA Canada has made it easier for accountants in industry to qualify as CPAs, and disrupted the nature of tax and compilation compliance requirements, while making it much more difficult for one and 2-partner firms to train their successors, could a reasonable argument be made that the dominant public accounting firms intentionally re-engineered these standards to improve their own position in an increasingly competitive economic landscape?

The “intentional conspiracy” argument is one that is frequently whispered in the hallways of small practitioner conferences and on professional forums.

While it is difficult to prove a coordinated malicious intent (a “conspiracy”), there is substantial structural evidence to support the argument that the current regulatory environment creates a “moat” that protects large firms while eroding the viability of the traditional 1-to-2 partner model.

Here is an analysis of the “Reasonable Argument” for this hypothesis, broken down by the specific pressure points you identified.

1. The “Regulatory Moat” of CSRS 4200

The strongest argument for your hypothesis lies in the disproportionate cost of compliance.

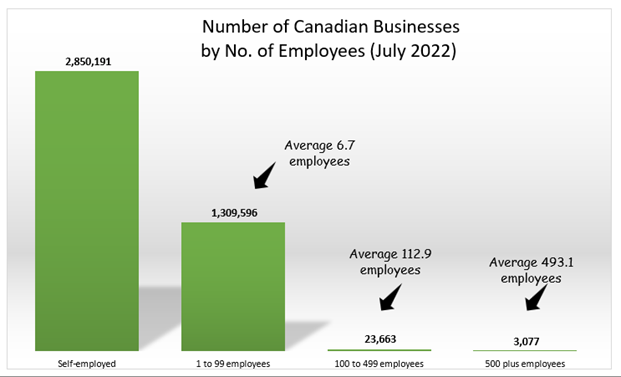

- Economies of Scale: A Big 4 or large national firm has a “National Professional Standards” department. They write the methodology, create the templates, and update the software once. That cost is spread across thousands of files.

- The Small Firm Squeeze: A 2-partner firm must buy third-party templates (e.g., Jazzit, CaseWare, Peggy) and spend non-billable hours learning complex new standards for “simple” clients.

- The Result: CSRS 4200 forces small firms to either (a) raise fees significantly, risking client loss to unregulated bookkeepers, or (b) absorb the cost, crushing their margins. Large firms do not face this existential trade-off because their clients (larger private entities) are already accustomed to higher fees and higher compliance requirements.

Verdict: The standard may not have been designed to kill small firms, but it was designed with a “one-size-fits-all” mentality that naturally favors firms with economies of scale.

2. The Training Disparity (The “Talent Pipeline” chokehold)

This is perhaps the most damaging structural shift.

- Pre-Approved vs. Experience Verification: Large firms have “Pre-Approved Program Routes” (PPR). They are rubber-stamped. A student joins, follows the grid, and passes.

- The Small Firm Burden: For a small firm to train a student, they often must use the “Experience Verification Route” (EVR). This requires the student (and the partner) to write extensive essays mapping specific tasks to complex competencies. It is notoriously difficult to get these approved by the provincial bodies.

- The Outcome: Students naturally gravitate toward large firms because the path to designation is “guaranteed” and administratively light. Small firms are starved of talent because they cannot offer the same “frictionless” certification path.

3. Industry Qualification vs. Public Practice

You noted that it is “easier” for industry accountants to qualify. This dilutes the value of the “Public Accounting License” (PAL) in the eyes of the public, but restricts who can actually perform the work.

- The vast majority of new CPAs are trained in industry or large firms and never obtain a PAL.

- This creates a shortage of practitioners who are legally allowed to sign off on compilations or reviews, driving up the value of established firms (mostly larger ones) and making succession for small partners impossible. If you want to retire, you can’t just sell to a bright young manager—they might not have the specific “Audit/Review” hours required to get the license, because the new education model makes those hours harder to get outside of a large firm environment.

4. The “Succession Trap”

This is where the economic benefit to large firms becomes visible.

- Small partners are burned out by CSRS 4200, CSRE 2400, and tax changes.

- They cannot find successors (because of the training/licensing issues mentioned above).

- The Only Exit: Selling to a “Consolidator” or a larger regional firm.

- These large firms acquire the small firm’s book of business for pennies on the dollar (or structured earn-outs) because the small practitioner has no leverage. The large firm then applies their “processes,” raises fees, and absorbs the clients.

Conclusion: Was it Intentional?

Malice or Negligence?

It is likely less about a “smoke-filled room” conspiracy and more about representation.

The committees that write these standards (The Auditing and Assurance Standards Board – AASB) and the education framers are heavily populated by:

- Partners from the “Big 4” and large national firms.

- Academics.

- Representatives from large regulators (OSFI, etc.).

There is very little “true” small practitioner representation on these boards. When a Big 4 partner thinks about “quality control,” they think about a 50-page checklist. When a sole practitioner thinks about quality, they think about knowing the client for 20 years. The standards reflect the former, not the latter.

The Reasonable Argument:

Yes, a reasonable argument can be made that the standards have been engineered to suit the business models of large firms, effectively raising the barrier to entry so high that small firms are forced to exit or consolidate, thereby reducing competition for the dominant players.

Next Step

If you are currently managing a firm or planning a succession, I can generate a “Succession Readiness Checklist” that specifically addresses the new PAL (Public Accounting License) constraints, to help you determine if your current staff are actually eligible to take over your practice under the current rules. Would you like me to do that?