How has that worked out?

What Did it Replace?

Before 1991, Canada relied on a federal sales tax known as the Manufacturers’ Sales Tax (MST). While both the MST and the current Goods and Services Tax (GST) are consumption taxes, they differ markedly in design and impact:

- Scope and Coverage

The MST was imposed mainly on domestically manufactured goods—a narrower tax base focused on production. In contrast, the GST—introduced in 1991—is a broad-based value-added tax that applies to almost all goods and services sold in Canada. This change expanded the tax’s reach, ensuring that most consumer spending contributed to federal revenues [2][4]. - Tax Cascading vs. Input Tax Credits

One of the key drawbacks of the MST was its cascading nature. Since it was levied at successive points in the manufacturing process without providing credits for taxes already paid on inputs, the MST could inadvertently “tax a tax,” inflating the effective tax rate on final products. The GST, however, is designed to be neutral regarding business inputs. It allows businesses to claim input tax credits for GST paid on business purchases, helping to avoid the cascade effect and reducing production costs, which generally benefits both businesses and consumers [4]. - Economic Efficiency and Policy Goals

The move from the MST to the GST was part of modernizing Canada’s tax system. While the MST contributed significant revenue, its narrow base and cascading mechanism led to distortions in production costs and competitiveness. The GST’s broader base and credit mechanism were intended to promote economic efficiency and more equitable tax incidence, aligning Canada’s system with those of many other industrialized nations [4]. - Rates and Administration

Historically, the MST’s rates varied depending on the product and the manufacturing process, and its administration was often seen as cumbersome due to the lack of uniformity. The GST, set at 5% today, is uniformly applied across nearly all provincial jurisdictions (with some provinces combining it with their own sales tax to form the Harmonized Sales Tax, or HST). This consistency helps simplify compliance and enhances the predictability of federal revenue collections [2].

In summary, while the MST was a federal sales tax targeting a specific segment of economic activity (manufacturing) and operated in a cascading manner, the current GST is a comprehensive value-added tax with input tax credits that avoids double taxation. The GST was designed to be more efficient and equitable, reflecting lessons learned from the limitations of the previous tax system.

(Note: As a former tax auditor and public accountant I almost never dealt with the manufacturer’s sales tax in about 10 years working with primarily small businesses.)

The Theoretical Rationale Behind the GST:

Sales taxes are often seen as regressive because everyone pays the same rate regardless of income, meaning that lower-income households end up dedicating a larger share of their earnings on taxed goods and services. Despite this, governments lean on sales taxes for several key reasons:

- Broad and Stable Revenue Base:

Sales taxes capture contributions from virtually every consumer since nearly all purchases of taxable goods and services are included. This broad base makes the revenue stream predictable and stable, which is critically important for funding essential public services and infrastructure[2]. - Ease of Administration:

Collected directly at the point-of-sale, sales taxes are straightforward to administer. This minimizes compliance and collection costs, reduces the opportunities for tax evasion, and alleviates the bureaucratic burden compared to more complex income-based tax schemes[2]. - Simplicity and Low Compliance Costs:

Because sales taxes are applied uniformly to most purchases, they are simpler for both businesses and tax authorities to manage. This simplicity can mean lower administrative expenses, which is an advantage in maintaining an efficient tax system. - Consumption Versus Income Taxation:

While it’s true that sales taxes take a larger percentage of income from lower earners on an annual basis, economists sometimes argue that evaluating tax fairness over a lifetime—but rather on lifetime consumption—can paint a different picture[3]. People tend to save and spread their consumption over the years, which may mitigate the regressive appearance when looking at long-term economic behavior. - Targeted Mitigations:

Many governments design sales tax systems with measures to lessen the regressive impact. For instance, they might exempt necessities such as basic groceries or children’s clothing, or offer rebates and credits to low-income households. These adjustments help balance the need for revenue with concerns about equity[4].

In essence, while sales taxes have a regressive nature by design, their administrative efficiency, broad applicability, stability, and the potential for targeted mitigations make them an appealing choice for governments looking to generate a large and reliable revenue stream to fund public programs.

(Note: while small businesses did have to deal with provincial sales taxes prior to the implementation of the GST, almost none had to deal with the complexities of the manufacturer’s sales tax.)

The Reality

Today virtually every small business must deal with the complexities of Canada’s GST.

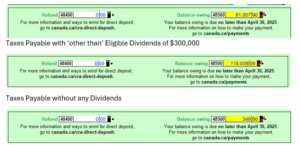

Every purchase made by the business is typically subject to GST. But at what rate?

That means having access to the actual invoice when most often transactions are imported from a small business’s business bank account or the owner’s credit card.

The input tax credits which are recoverable, vary depending on where the seller’s ‘place of supply’ is. Rates vary from between 5% and 15% depending on the province of the vendor.

Similarly, companies located in one province and selling to someone in another province must consider the ‘place of supply rules’ when preparing an invoice. Small businesses doing their own bookkeeping using Quickbooks, are seldom able to figure it out properly.

They must also consider ‘exempt supplies’ or ‘zero-rated supplies’…

| Differences in the tax status | ||

| Tax status | What this means | If you are a GST/HST registrant, then |

| Taxable supplies (other than zero-rated) | Most property and services supplied in or imported into Canada are subject to GST/HST. For everything except zero-rated or exempt supplies, you must determine which GST/HST rate to charge. Example – Taxable supplies (other than zero-rated) | you charge and collect the GST/HST on the supplies that are made in Canadayou may be eligible to claim input tax credits (ITCs) to recover GST/HST paid or payable |

| Zero-rated supplies | Some supplies are zero-rated under the GST/HST. This mean that GST/HST applies to these supplies at the rate of 0%. Example – Supplies taxable at 0% | GST/HST of 0% is charged, which means you do not collect the GST/HST on these suppliesyou may be eligible to claim ITCs to recover GST/HST paid or payable |

| Exempt supplies | Some supplies are exempt from the GST/HST. GST/HST does not apply to these supplies. Example – Exempt supplies | you do not charge or collect the GST/HSTyou generally cannot claim ITCs to recover GST/HST paid or payable If you are a public service body that makes exempt supplies, you may be eligible to claim a public service bodies’ rebate for the GST/HST paid or payable on expenses related to making exempt supplies whether or not you are registered for the GST/HST. For more information, see Guide RC4034, GST/HST Public Service Bodies’ Rebate. |

It may just be me, but I find GST auditors particularly difficult to deal with.

In one recent situation, my client was a small Canadian private corporation controlled by a US parent. They had about 10 sales staff, split between Ontario and British Columbia. So while the company’s charges to their US parent should be theoretically exempt, they were subject to GST on purchases – in more than one province.

In order to meet the requirements of transfer pricing tax rules, they had to ensure that intercompany fees charged by the two entities did not offend transfer pricing rules. I had advised them earlier to put some documentation in place in the way of contract for services. It wasn’t really required – but nice to have.

Before the CFO could have the contract written up, he left the company.

Then, CRA began an audit of the company’s GST filing and requested a copy of the written agreement – which of course did not yet exist.

In truth, a contract does not have to written to be valid.

However clearly, the GST auditor’s supervisor demanded it.

I was able to provide CRA’s own guidance with respect to transfer pricing that I had previously sent to the company. That was not adequate for the auditor.

My instincts tell me that officials in one CRA department (GST) are attempting to deny benefits of input tax credits based on a potential flaw in advice from another group (transfer pricing) within the CRA.

Of course, if we got rid of the GST, all 13 provinces in territories would revert to their own provincial or territorial taxes, making the situation worse.

How is that for simplicity?

BACKGROUND ON TRANSFER PRICING AGREEMENTS

There’s no “one‐size‐fits‐all” percentage recommended by the Canadian tax authorities or by widely accepted transfer pricing guidelines. Instead, both Canada’s Revenue Agency (CRA) and global best practices require that intercompany transactions—such as charges from a Canadian subsidiary to its US parent—be set at arm’s length. In practical terms, this means that the markup should be determined by a rigorous comparability analysis looking at similar transactions between independent parties.

For example, if you’re using a Cost Plus method (a common approach for service or cost-based transactions), you would add a markup to the incurred costs that an independent supplier would typically earn on a similar service. This “normal” markup can vary by industry, the functions performed, the risks assumed, and the specific market conditions. In some industries, benchmarks might suggest markups in the ballpark of 5% to 20%, but the exact percentage will depend on the facts and circumstances of each case rather than on a fixed “recommended” number.

Because the CRA (and the IRS, in the U.S.) expects that the pricing reflects what truly independent parties would agree upon, companies usually rely on detailed functional analyses and external comparables (from databases or industry studies) to establish their markup. Detailed contemporaneous documentation is crucial in order to demonstrate that the transfer prices are indeed set on an arm’s length basis, potentially supported by one of the standard transfer pricing methods (Cost Plus, Resale Price, CUP, etc.) .

In summary, rather than using a predetermined markup, you should conduct a robust analysis of comparable uncontrolled transactions to determine the applicable markup. Given the complexities—and the fact that these markups can vary widely—it’s advisable for companies to work closely with transfer pricing specialists or tax advisors who can tailor the analysis to the specific details of your business and industry.

Some additional points you might explore include:

- How different transfer pricing methods (e.g., CUP, resale price, cost plus) might impact your approach.

- The importance of continuous benchmarking and documentation to adjust the markup as market conditions change.

- How other jurisdictions (like the US under IRS guidelines or OECD recommendations) handle similar intercompany pricing issues.