As a professional accountant with more than 3 decades of experience – including 5 years with the CRA as an auditor and 5 years with a Big Four firm as a tax specialist in SR&ED, I began dealing with a Silicon Valley-based financial startup, handling the tax compliance for their small Canadian subsidiary.

Three years after I started, the company outsourced its internal finance and accounting services to a venture-backed FAAS (Finance As A Service) company, headquartered in Austin, Texas..

I began to suspect the quality of the work being done by the outsourced service partner, so I took a look at their profile on Crunchbase –

Crunchbase.com is a leading online platform that provides data and predictive intelligence on private companies, startups, investors, and funding activity. It’s widely used by entrepreneurs, venture capitalists, analysts, and business professionals to track company growth, investment trends, and market opportunities.

According to Crunchbase, the FAAS provider was founded in 2006 and has grown to between 1001 and 5000 employees. By any measure, that’s a large company.

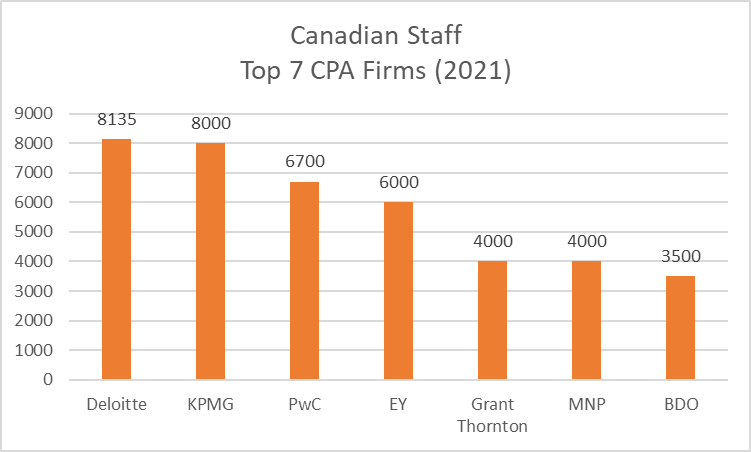

A few years ago, I analyzed the top 7 accounting firms in Canada by revenue and employment. Based on this data, the FAAS service is quite a large firm.

Next, I asked Gemini to look at the size of the top 100 CPA firms in the US:

“Firms Outside the Big Four: Looking at the other firms in the Top 100, a firm with revenues below the $1 billion mark typically has a US workforce ranging from a few hundred employees up to several thousand (e.g., firms like RSM, BDO, or Grant Thornton often have tens of thousands of employees, while firms ranked near the bottom of the Top 100 may employ only a few hundred people).”

These numbers align with what I would expect based on my own experience.

But, to be clear, this particular FAAS company is not a CPA or CA firm. That means that it avoids professional regulation and oversight.

The FAAS-appointed controller told me that my client’s financials had been ‘audited’. However, that’s doubtful since the point of using a FAAS service is to use wage arbitrage to reduce labour costs. And unless they engaged an independent audit firm, no financial audit was conducted. Presumably, the FAAS provider itself performed an ‘internal audit’. But that isn’t the same thing, since an external audit requires independence.

The reason I began to question the idea that financials were actually audited independently was that too much of the company’s Canadian payroll was being deferred – ostensibly pursuant to US GAAP (specifically ASC 340-40, Other Assets and Deferred Costs—Contracts with Customers).

ASC 340-40 requires the company to capitalize incremental sales commissions for sales where the related revenue will be recognized in a subsequent year. Once capitalized as an asset, the commission cost must be amortized (expensed) over the period that the related goods or services are transferred to the customer.

In this case, fully 57% of prior year wages were capitalized. What’s more, there was no apparent amortization of these costs. My discussions with management indicated that only one of the company’s approximately twelve salespeople was involved in complex sales that might require capitalization. The rest of the sales team was simply arranging sales meetings for technical sales staff. Normally, this wouldn’t meet the threshold for deferral.

The most obvious conclusion was that the company wanted to improve the ‘apparent profitability’ by deferring what should have been expenses, with no corresponding amortization against long-term sales contracts.

This led me to the VP of Finance’s LinkedIn page.

He earned a CA designation in India, then worked for 3 years and 10 months, eventually becoming a partner at a 2-partner CA firm in Ahmedabad.

Next he worked with a Canadian CPA firm in Ontario for two months. This was followed by two short stints as a controller (3 to 4 years in total) – one of which was acquired by the particular FAAS service provider I was interested in.

I couldn’t help wondering how this experience prepared him to lead a ‘Global FAAS service’ as VP Finance, with more than a thousand employees (if Crunchbase can be believed).

It’s also a little surprising that he earned a CPA designation from Ontario so quickly (more about that in a future article).

As a result of these concerns, I was faced with a challenge.

The prior year’s financials had been prepared on a cash basis and adjusted to an accrual basis to conform with Canadian tax requirements. The Canadian tax department conducted a GST audit to determine whether intercompany payroll charges for sales and marketing activities, along with the related transfer pricing adjustments, would be subject to GST (Canadian value-added tax).

I was in the process of finalizing the audit and had reached an agreement with the tax auditor to vacate their proposed assessment of $112,000. The final result was still subject to the review of the GST auditor’s manager.

However, the new ‘audited’ financials contained significant prior period adjustments, including $717 thousand in deferred commission and an increase in the intercompany payable of $194 thousand. This latter adjustment was the very item that had been the subject of the GST audit.

My challenge was:

Should I maintain a reconciliation – something like a consolidation worksheet – to align US GAAP with Tax-Basis reporting?

“A consolidation worksheet is a preparatory tool in financial accounting used to combine the financial statements of a parent company and its subsidiaries. It organizes trial balances, adjustments, and elimination entries so that consolidated financial statements can be produced accurately, without double-counting or distortions from intercompany transactions”.

The optics of amending a prior period that has been subject to a tax audit are horrible.

What’s more, adjustments appeared to have been done based on a very ‘optimistic’ interpretation of US GAAP. Would these actually survive the due diligence process of a sophisticated investor?