In 2015 the Big 4 accounting firms employed about 75,000 staff in low-cost delivery centres (i.e. India, Philippines, Poland, Argentina, etc.). By 2025 that had increased to a headcount of more than 285,000.

According to Microsoft’s CoPilot AI service:

“A typical audit file for a Vancouver-listed issuer might be staffed 30 % in Canada, 50 % in India, 20 % in the Philippines, with rolling 24-hour hand-offs.”

At the same time, CPA regulatory bodies’ publications in both the USA and Canada are complaining about the shortage of new recruits and the lack of interest in the CPA designation.

Why the sharp rise in offshoring among Big 4 firms?

- Talent pinch: western graduate cohorts are shrinking while demand for data-heavy audit, ESG and cyber work is exploding.

- Margin pressure: fee caps on commoditised compliance work push firms toward 30-50 % labour-arbitrage saves.

- Remote-first mentality: once Covid proved that auditors and litigators could review files from the kitchen table, the psychological barrier to a Bangalore or Cebu location largely vanished.

- Tech stack convergence: the Big 4 and large law firms now run the same cloud-based work-paper, tax-prep or e-discovery platforms globally, making geographic placement almost irrelevant.

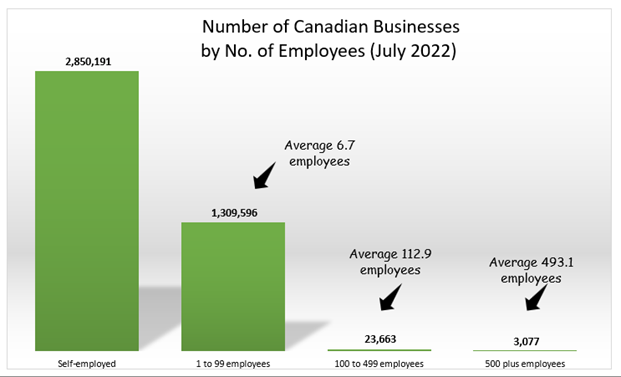

While about 52% of the Big 4 firms’ revenue derives from auditing and management consulting, those two lines of service are irrelevant for most of Canada’s accounting services industry. The smallest 52,336 firms earn about 97% of their revenue from tax and compilation work.

Despite this, even though their work is highly valued by their small business clients, these small firms can’t meet competency requirements – which were modified to align better with the needs of the largest firms.

Clearly, small firms need to look at different business models.

BACKGROUND (Courtesy Microsoft’s CoPilot AI Service)

Is offshoring becoming more common in large professional services firms?

Yes — and the pace has shifted from “interesting experiment” to “default operating model” for most Tier-1 accounting, tax, legal and consulting networks.

1 The headline numbers

| Indicator | 2015 | 2020 | 2024-25 (latest public figures) |

| Big 4 head-count in low-cost delivery centres (India, Philippines, Poland, Argentina, etc.) | ≈ 75 000 | ≈ 160 000 | > 285 000 (Deloitte 120 k, EY 70 k, PwC 55 k, KPMG 40 k) |

| % of global audit hours performed offshore | < 10 % | 18 % | ~30 % |

| Share of law-firm Am Law 100 billable hours handled by “captive” Indian ALSPs | ~ 4 % | 9 % | 14 % |

| Canadian Top-10 accounting firms with an owned or dedicated offshore pod | 1 / 10 | 4 / 10 | 8 / 10 |

(Compiled from annual reports, firm press releases, and ALM Intelligence surveys, 2020-25.)

Why the sharp rise?

- Talent pinch: western graduate cohorts are shrinking while demand for data-heavy audit, ESG and cyber work is exploding.

- Margin pressure: fee caps on commoditised compliance work push firms toward 30-50 % labour-arbitrage saves.

- Remote-first mentality: once Covid proved that auditors and litigators could review files from the kitchen table, the psychological barrier to a Bangalore or Cebu location largely vanished.

- Tech stack convergence: the Big 4 and large law firms now run the same cloud-based work-paper, tax-prep or e-discovery platforms globally, making geographic placement almost irrelevant.

2 How the model is evolving

From “outsourcing” to “captive GCC”

• 2025 vintage centres are typically wholly-owned Global Capability Centres (GCCs) rather than third-party BPO vendors.

• The centre handles multiple service lines (audit analytics + R&D tax + managed cyber) under common risk controls.

Second-tier hubs mushrooming

• Talent saturation in Bengaluru and Manila is pushing Big 4 firms to Tier-2 Indian cities (Pune, Hyderabad, Kochi) and to emerging sites such as Colombo, Ho Chi Minh City and Guadalajara.

Work moving up the value chain

• Early waves were pure tick-and-tie tasks; now we see complex transfer-pricing calculations, IFRS technical reviews and even first-draft legal memos prepared offshore.

• PwC’s Acceleration Centers report that > 40 % of staff hold a CPA, CFA or law degree equivalent.

Blended delivery norms

• A typical audit file for a Vancouver-listed issuer might be staffed 30 % Canada, 50 % India, 20 % Philippines, with rolling 24-hour hand-offs.

• Project-management toolkits (e.g., Workday PSA, KPMG Clara, Thomson One) auto-route subtasks to the cheapest qualified time-zone.

3 Risks firms are wrestling with

| Risk | Mitigation in 2025 builds |

| Data sovereignty & client consent | “Ring-fenced” GCCs inside ISO 27001 / SOC 2 Type 2 facilities; separate Azure tenants; contractual addenda for PII localisation. |

| Regulatory blow-back (e.g., PCAOB audit work-paper access) | On-shore partners retain sign-off; regulators given site-access audit trails; dual-hosting of key evidence. |

| Talent retention abroad (churn > 24 %) | Equity programmes, CFA/CPA sponsorships, and internal job-mobility to western offices. |

| Cultural & communication gaps | Mandatory “follow-the-sun” scrum rituals; Gen-AI language assistants embedded in Teams/Slack. |

4 What it means for a Canadian professional-services firm in 2025

- Client expectations have reset. If you pitch a cross-border M&A due-diligence and your competitor can quote 18-hour turnaround by leaning on Manila analysts, you must justify staying 100 % on-shore.

- Labor-law arbitrage intersects with Canadian ESA exemptions. Your BC-based junior accountants are ESA-exempt, yet still cost 2-× their Delhi peers. Boards now ask why.

- Capability not just cost. Offshore pods are becoming centres of excellence for ESG data tagging, AI model audits, and mass-contract repapering—skills scarce at home.

- Career path recalibration. First-year staff in Victoria may now supervise a six-person Hyderabad work-cell by year two; your training and leadership curricula must adapt.

Watch-list for 2025-26

• Indian Finance Bill 2025 proposes a 2 % “signing-partner PE” levy on foreign audit fees—could dent the arbitrage.

• EU’s proposed Cybersecurity Certification Scheme (EUCS) may restrict off-EU processing of sensitive client data.

• Generative-AI copilots are predicted to eliminate 15-20 % of low-level offshore hours by 2027, pushing centres further up the value curve rather than destroying them.

Bottom line

Offshoring in large professional-services firms is no longer optional or limited to back-office chores; it is now embedded in core client delivery, scaling rapidly in head-count and sophistication. Any firm that wants to stay cost-competitive and talent-resilient needs a clear offshore (or “right-shore”) playbook—balanced by robust controls, career-architecture tweaks and frank conversations with regulators and clients about where the work is really done.

Happy to dig into location-screening criteria, build-operate-transfer models or the hurdle rate at which offshoring stops making sense for mid-tier Canadian practices.