EXAMPLE: Taxpayer with total income before dividends of approximately $30,000

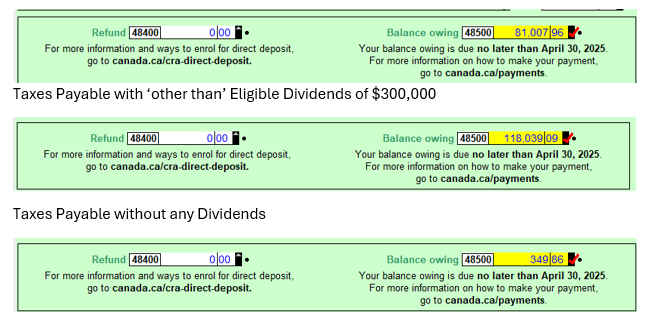

Actual Taxes Payable with Eligible Dividends of $300,000

The tax rate on eligible dividends is much lower than the rate on “other than eligible dividends” (see table below). However, there must be sufficient “general rate income pool” (GRIP) to pay eligible dividends from.

| Dividends | Income | Tax Payable | Attributable to Dividends | Related Tax | Tax Rate on Dividends |

| None | $ 30,000.00 | $ 349.86 | $ – | ||

| Eligible | $ 330,000.00 | $ 81,007.96 | $ 300,000.00 | $ 80,658.10 | 26.9% |

| Not Eligible | $ 330,000.00 | $ 118,039.09 | $ 300,000.00 | $ 117,689.23 | 39.2% |

| Eligibile | $ 10,030,000.00 | $ 3,265,647.53 | $ 10,000,000.00 | $ 3,265,297.67 | 32.7% |

T5s for dividends must be filed by February 28th of the following year to avoid a penalty. However, the maximum penalty for a single late-filed T5 is just $100. Unfortunately, when we do the accounting at the end of the year it is difficult to know what the GRIP was when the dividends were theoretically paid (or at least deemed paid), on December 31st since the accounting and tax work had not yet been completed.

So, I dutifully issued the T5 on February 28th as being “other than eligible” dividends.

By the time I realized there was sufficient GRIP, I quickly filed an amended T5 (and T5 Summary). However, this was after the February 28th filing deadline. The CRA in their wisdom, determined that was not in fact an “amended” dividend filing, but a new filing and hence late-filed.

Since the penalty is trivial in relation to the tax savings, it seems counter-productive to argue that they are mistaken since the cost of making the argument is much greater than the penalty. What’s more, their determination was possibly correct in any event.

Taxes Payable with $10,000,000 in Eligible Dividends